To read the original post, click here

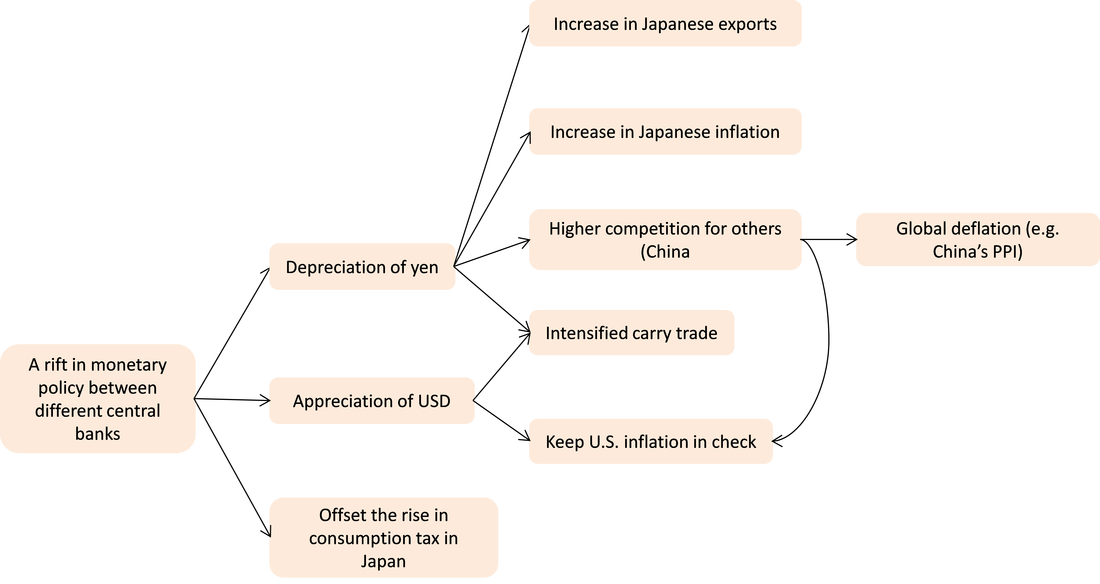

Here is a flow chart of the main ideas presented in the article:

I want to discuss a problem related to the depreciation and export relationship in Japan.

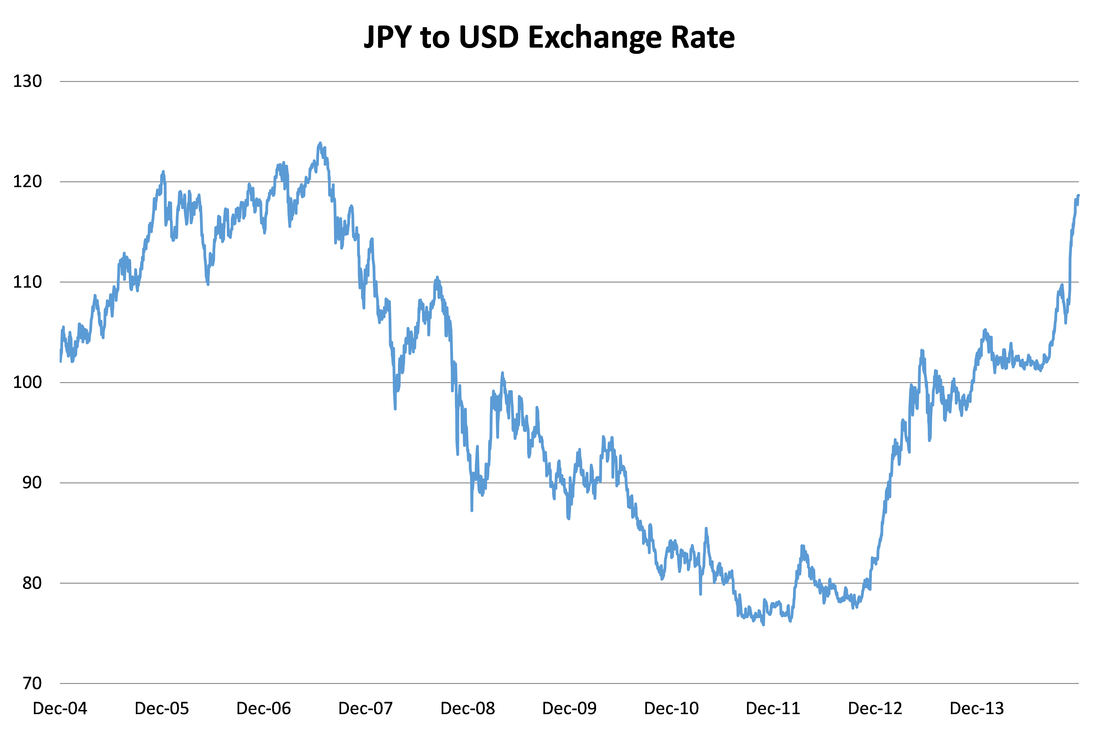

Firstly, this article claims that a depreciation in the JPY should increase exports. Here is a chart of the JPY to USD chart from The Bloomberg.

Firstly, this article claims that a depreciation in the JPY should increase exports. Here is a chart of the JPY to USD chart from The Bloomberg.

As we can see, there was an appreciation from about 2006 to 2011, followed by a depreciation from 2011 onward. The volume of exports from 2011 to 2014, however, had not increased dramatically, despite the depreciation of the Yen.

Source: Bloomberg

Why could this be? Many people claim that it has to do with the structural rigidities of Japan (i.e. Japan is no longer producing what people want to buy).

Why could this be? Many people claim that it has to do with the structural rigidities of Japan (i.e. Japan is no longer producing what people want to buy).

RSS Feed

RSS Feed